TradFi Will Rule Onchain FX, not Crypto

Central Banks are smarter than you think

The entire CT debate around FX is fixated on a flawed comparison between USD and non-USD stablecoin dominance.

The arguments roughly fall into two camps:

Camp 1 argues that there is simply no demand or liquidity for non-USD stablecoins. People use USD stablecoins because of the strength of the dollar or its reliability as a store of value in weaker economies.

Whereas Camp 2 makes the case for the lack of FX infrastructure, making it impossible for non-USD stablecoins to break into the scene. AMMs are inefficient in Spot FX, and we simply have no infra for FX Swaps.

While both sides make strong arguments, they are missing the full picture.

It’s not a technical problem nor a volume problem to solve. FX doesn’t move $10T/day because it uses superior technology. The FX infrastructure has been built over seven decades through meticulous international collaboration while ensuring the safety and monetary sovereignty of nation-states.

The primary impediment for onchain FX is regulation.

You can not replace a rigid network based on trust and autonomy at the snap of the fingers.

Before I dive into the solution, a bit of context is necessary.

How the FX Network Was Built

The origin of FX goes back to the Bretton Woods conference in 1944, where 44 nations agreed to a fixed exchange rate system pegged to the US Dollar, which was in turn pegged to gold. This established the dollar as the vehicle currency for the world.

When the world moved to floating exchange rates in the 1970s, volatility skyrocketed, leading to the creation of SWIFT in 1973 to standardize messaging. But the most critical lesson came in 1974 with the collapse of Bankhaus Herstatt. The German bank failed after receiving payments in Deutsche Marks and couldn’t clear the corresponding US Dollars, leaving counterparties with massive losses. This “Herstatt Risk“ (settlement risk) traumatized the market.

Why Central Banks Are the Likely Winner

It took nearly 30 years to build a solution that a coalition of Central Banks would eventually agree on, thus the CLS system was launched in 2002.

Since its inception, CLS has added a total of 18 currencies to its network.

Major currencies (by FX turnover) like CNY (8.5%), INR (1.8%), TWD (1.2%), etc, are still missing from the CLS system.

The private stablecoin thesis assumes that central banks will sit idly by while private entities issue digital proxies of their national currencies. This ignores the geopolitical reality of monetary sovereignty, clearly reflected in existing infrastructures like CLS.

Bringing multiple central banks onto a single, permissionless ledger in its current stage is a diplomatic impossibility. No Central bank will ever relinquish its absolute control over monetary policy.

We’re already seeing significant constraints being put on stablecoins functions through MiCA, rendering pretty much all innovative solutions moot in the EU.

Strict Authorization: EMTs (single-currency stablecoins) can only be issued by authorized credit institutions (banks) or EMIs. This bars FinTech platforms without full banking licenses from issuing Euro stablecoins.

Capital Requirements: Issuers must hold significant capital reserves, separate from the reserve assets backing the token. This destroys the capital efficiency that made early stablecoins profitable.

Compliance Costs: The cost of compliance, including legal fees, audits, and dedicated staff, will amount to hundreds of thousands of Euros annually.

The result is market consolidation. Only large, incumbent banks (e.g., Société Générale’s EUR CoinVertible) can afford to play. These institutions have no incentive to facilitate permissionless FX markets.

The US nipped this problem in the bud with the GENIUS Act, creating clear guidelines for private stablecoins issuers to thrive. This act essentially ensured the continued dominance of USD-denominated private stablecoins for years to come, consequently bolstering the dollar hegemony.

However, that doesn’t mean international players are sitting idly by while the US unilaterally dominates the blockchain-based payment space.

Surveys of the G20 and Financial Stability Board (FSB) members show a distinct preference for CBDCs and strict stablecoin regulation. By 2025, 62% of FSB members expect to have fully aligned crypto-asset frameworks.

For Central Banks, the choice is clear: Do you run your economy on a private, uncontrolled rail (like Ethereum) using a private token (like Tether), or do you opt for something that allows you to remain the ultimate authority? The state will always choose the state.

Here is a list of initiatives international financial authorities have undertaken (and made significant advancements) over the last few years:

1. Project Guardian

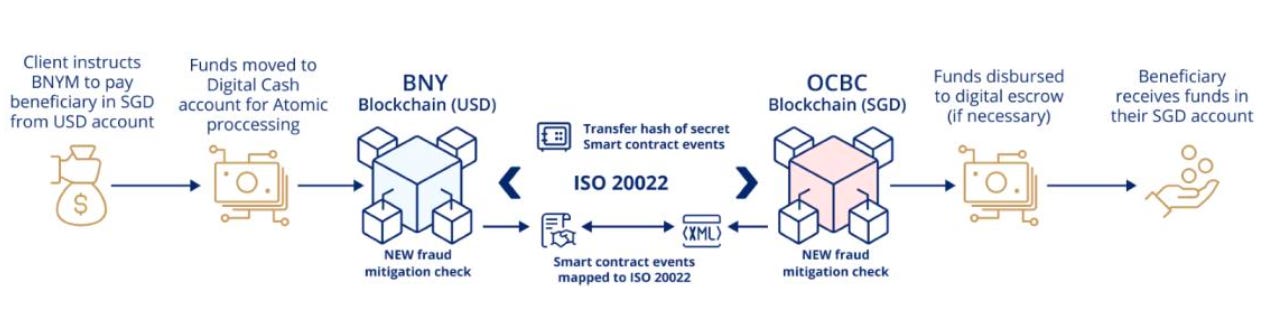

Project Guardian is one of the key initiatives undertaken by Ant International and ISDA, with contributions from MAS, OCBC, BNY Mellon, and HSBC, aiming to move toward using tokenised bank liabilities on shared ledgers to solve inefficiencies in cross-border FX settlements.

Guardian is taking an approach to address instant cross-border settlements from three fronts:

a liquidity swap model where existing bank liabilities are settled by a designated entity (Ant) that swaps tokenised deposits from different issuing banks (e.g., swapping Tokenised SGD for Tokenised USD) to enable instant cross-border payments.

The end result will be increasing the number of liquidity providers, therefore scaling up the settlement volume; essentially creating liquidity hubs for network banks to settle transactions immediately.Another initiative proved that two completely different private bank ledgers could interoperate. Using Hash-Time Locked Contracts (HTLC), they are aiming to process payments without needing a single shared platform, preserving the autonomy of each bank’s ledger.

The originating bank initiates a transaction as they would today, then passes a message via a bilateral connection to the beneficiary’s bank (or correspondent). The payment message will include a secret, which in turn unlocks the smart contract holding the funds in escrow. Once the funds are unlocked from escrow, they are credited to the beneficiary’s account in tokenised deposit form, and then made available for “last mile” pay-out through traditional instant payment rails.

The final and most important initiative that Guardian has undertaken is to upgrade the ISDA framework to facilitate Onchain FX. ISDA has been asked to develop industry-standard documentation to enable FX spot/forward/swap transactions to be settled using deposit tokens under the ISDA Master Agreement, via model “Additional Provisions.”

These Additional Provisions will be plugged into existing ISDA FX documentation architecture (1998 FX Definitions, and where relevant 2021 Definitions). It’ll assume a settlement setup compatible with the pilots (e.g., a liquidity provider holding pools of tokens from participating banks and facing users via FX confirmations under an ISDA Master).

ISDA will also likely consider changes such as the definition of “Business Day” for 24/7 settlement, plus explicit definitions/handling of tokenised deposits.

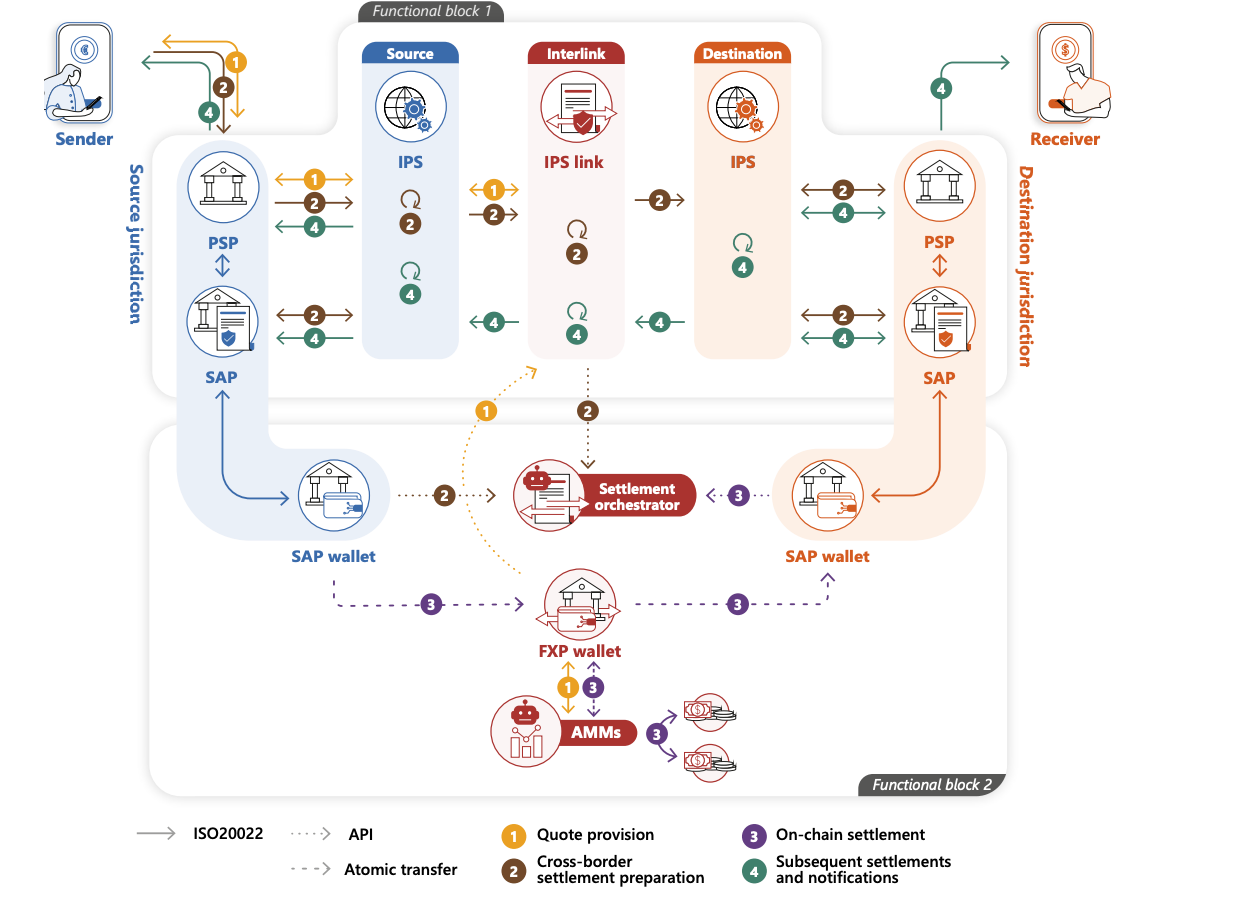

Project Rialto

Project Rialto is perhaps the clearest example of TradFi co-opting crypto technology to solve fiat problems. It targets the inefficient retail remittance market by replacing correspondent banking chains with an automated layer.

Rialto is a concentrated effort led by the BIS Innovation Hub and supported by the Central Banks of France, Italy, Malaysia, and the Monetary Authority of Singapore.

Rialto is explicitly adopting the AMM model instead of relying on manual dealer quotes; it uses liquidity pools and algorithmic pricing to execute currency swaps instantly using wCBDCs.

This eliminates credit risk entirely, offering a “risk-free” settlement asset that private stablecoins cannot match. It connects domestic Instant Payment Systems (IPS) directly, allowing a sender in one country to pay instantly to a receiver in another, with the complex FX conversion handled automatically in the middle layer.

mBridge

mBridge is another international coalition of Central Banks (China, HK, Saudi Arabia, UAE, and Thailand) working towards removing frictions in Central Bank operations.

If Rialto is the retail solution, mBridge is the geopolitical wholesale solution. It represents a fundamental restructuring of how central banks interact, bypassing the traditional correspondent banking system entirely.

mBridge allows central banks to transact directly on a shared ledger. This removes the need for bridge currencies (like the USD) in regional trade, allowing for direct peer-to-peer sovereign settlement.

JP Morgan’s Kinexys (formerly Onyx)

The abovementioned initiatives are overseen by Central Banks and other monetary authorities, whereas Kinexys is owned and operated by JP Morgan.

With their $4T in AUM, JP Morgan has shown that a private centralized ledger is not only possible but extremely useful. They have so far processed $1.5T, with >$2B average daily volume, plus 10x YoY growth in payment transactions using Kinexys.

Kinexys operates as a single-bank ledger, allowing unmatched speed and efficiency because settlement occurs on the books of a single trusted entity rather than across a fragmented network.

Kinexys is now moving into Onchain FX Settlement (starting with USD and EUR). BMW became the first company to carry out an FX transaction on Kinexys last December.

Primary Constraints for Solving FX in EM Countries

Despite good intentions, one of the major misconceptions that I see plaguing the Onchain FX space is the tendency to overlook economic reality when it comes to solving FX in the EM.

It’s going to be an exercise in futility for crypto platforms to try to replace USD as the bridge currency and connect two EM currencies directly onchain.

You can’t simply enable EM currency pairs in your FX platform and hope that those countries rush in to use it. The “build it and they’ll come” model doesn’t work here.

The Gravity Model of International Trade states that trade volume is proportional to the economic size of two countries. FX liquidity is a derivative of trade. If Nigeria and Mexico only trade $20 million worth of goods per year, there is no natural demand for a market maker to hold inventory of Naira and Pesos.

You can’t create $10 billion of FX liquidity if the two countries don’t trade in billions of dollars.

Because the trade flows don’t exist, the liquidity pools on-chain will remain empty. The reason these markets rely on the USD as a bridge is not that the plumbing is broken; it is because the dollar is the only asset liquid enough to bridge the gap between two disconnected economies.

Closing Thoughts

We are witnessing a “great co-option” of crypto-native innovations. The concepts pioneered by DeFi, like AMMs, atomic settlement, and shared ledgers, are being stripped of their decentralized ideology and integrated into the sovereign machinery of global finance. Initiatives like Rialto, mBridge, and Kinexys show that the problem isn’t the technology, but controllability.

The FX market of the next decade will indeed move onchain, but it will not be as open, permissionless, or decentralized as crypto natives envisioned. It will be a highly regulated, permissioned ecosystem where central banks and GSIBs retain control, leveraging the speed of blockchain while maintaining the safety of the state.

The irony is not lost on me that the movement started by cyberpunks to create an alternative financial paradigm is now being subsumed by the same monster it was created to defeat.

Nice share mate