Unsecured Lending Onchain is Hard

We can't beat banks like this

I have been studying stablecoins for the last 7 months like a madman. In this period, stablecoin companies have raised hundreds of millions of dollars, launched robust payment solutions, and managed to scare the crap out of archaic financial systems like SWIFT and ACH.

But one thing hasn’t changed at all. Unsecured lending onchain.

The US unsecured loan market is a $3+ trillion leviathan. If you layer on private credit and various forms of business financing, that number swells closer to $10 trillion.

It is the largest, most inefficient capital market on the planet.

For years, the primary argument for Stablecoin adoption has been simple: Stablecoins are superior rails. They are cheaper, faster, and radically more transparent than the existing TradFi systems.

By all logic, stablecoins should have swallowed this market whole.

But they haven’t. We are not even close to making a decent claim on it.

We have built excellent casinos and robust pawn shops (over-collateralized lending platforms). But we haven’t figured out how to give a business a loan based on its reputation or its cash flow without forcing them to lock up 150% of the value in ETH.

Solving the unsecured lending problem onchain is a surefire way to onboard the next billion users on the blockchain and unlock a multi-trillion-dollar industry.

But to get there, we have to stop talking about yield farming and start answering the hard questions:

How do we define Creditworthiness?

What is the legal recourse when a borrower defaults?

Who regulates this?

Addressing The Core Challenge

Interest Rate

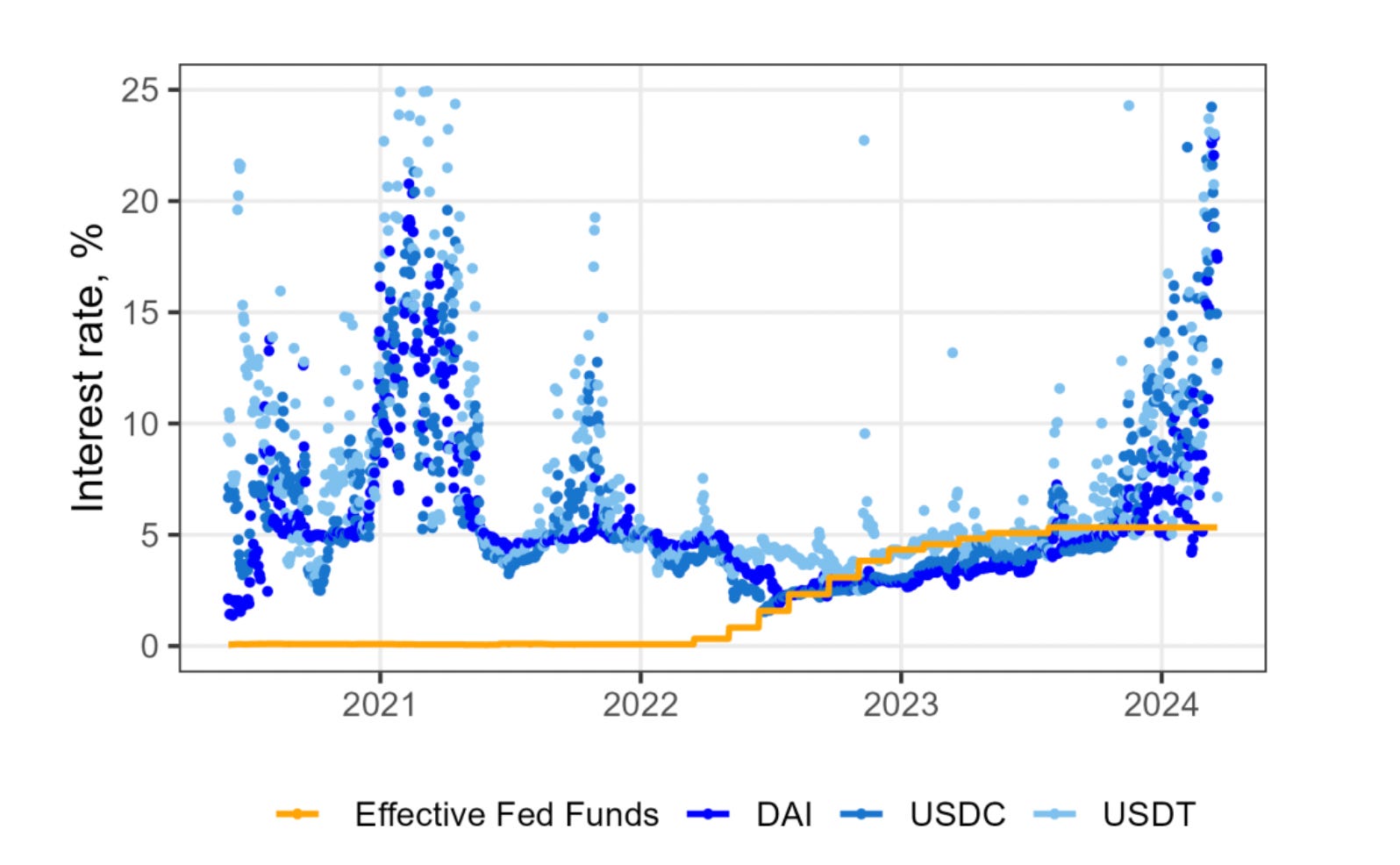

For the last two cycles, DeFi interest rates were a disaster. Completely disconnected from reality, driven by degen demand. When you could make 100% APY going long on a meme, you didn’t care if borrowing costs were 20%.

That made onchain credit useless for a real business. No business will ever pay 20% interest onchain when they can secure the same loan for single-digit rates.

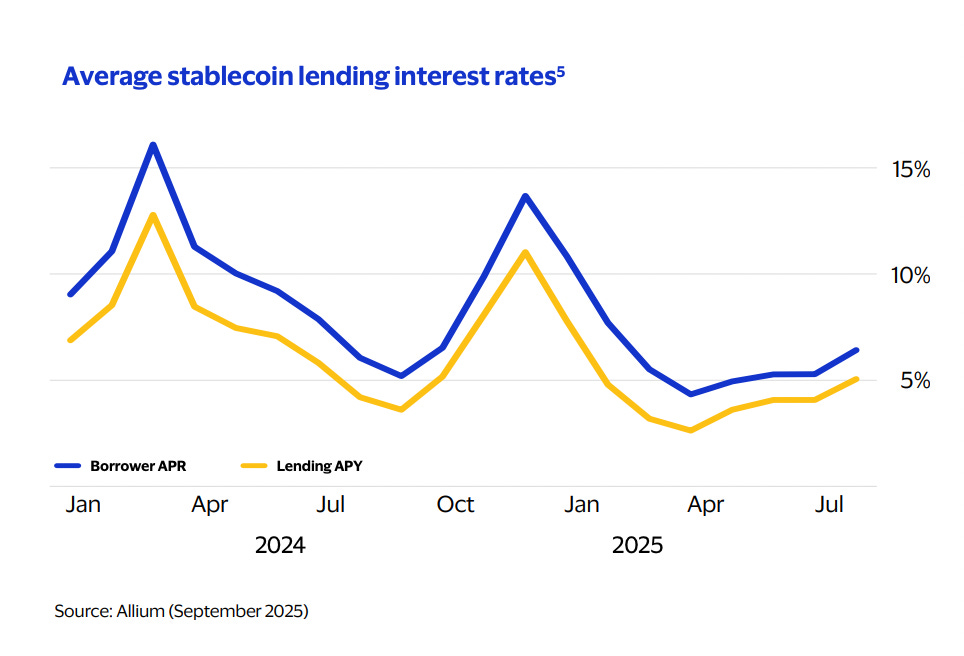

But look at the data from August 2025.

According to Visa’s onchain lending opportunity report, the spread has collapsed.

Borrowing Rate (APR): 6.4%

Lending Rate (APY): 5.1%

Spread: 1.3%

At 6.4%, on-chain capital is fairly competitive with a traditional bank line of credit.

The bottleneck has shifted. The problem is no longer economic.

Subprime Borrowers

The other part of the problem is the lack of willing prime borrowers.

The unsecured lending market is riddled with subprime borrowers from high-risk trading firms or companies based in EM economies paying an interest lower than their own government bond yields.

Given the lack of clear guidelines and trust around stablecoin borrowing, prime borrowers (high revenue, high cashflow businesses) have so far stayed out.

This creates a self-perpetuated cycle of misery for lending protocols.

Lend to subprime borrowers at low rates → Borrowers default → Find out legal recourse is close to none → Pivot to secured lending or Go out of business

The ultimate goal is to bring prime borrowers into the fold and create financial incentives that align with borrowers’ expectations and lenders’ risk profile.

Business lending is risky as it is, without introducing added variables such as anonymous borrowers or unclear financials.

In this article, I analyze a few of the most notable lending protocols and their efforts on debt recovery from defaulters. And in general, how they approach unsecured lending.

Attempts at Uncollateralized Lending

The first generation of unsecured lending protocols failed because they ignored a fundamental law of finance: Lending is easy, collecting is hard.

In 2022, protocols like Maple and Goldfinch operated on a “delegate” model. They trusted third-party assessors to vouch for borrowers. But when the market turned, these protocols discovered the enforcement gap.

If a borrower defaults on Aave, the smart contract liquidates their ETH in seconds. If a borrower defaults on an unsecured loan, you are forced offchain into legal purgatory.

Faced with this reality, the market bifurcated. Players either pivoted to fully secured lending (Maple) or fully outsourced underwriting (Goldfinch).

1. Maple Finance

Maple Finance is the definitive case study on why “trust” is not a scalable strategy.

In 2022, Maple was hit by the $36 million Orthogonal Trading default. Orthogonal misrepresented their exposure to the FTX collapse, hiding losses for weeks.

The aftermath exposed the fatal flaw of unsecured DeFi.

On-Chain: There was no kill switch to recover the funds.

Off-Chain: Lenders were forced to hire Kroll as liquidators and fight in the British Virgin Islands High Court.

Recovering assets through a lengthy legal battle in a foreign country is simply unfeasible for a small DeFi protocol.

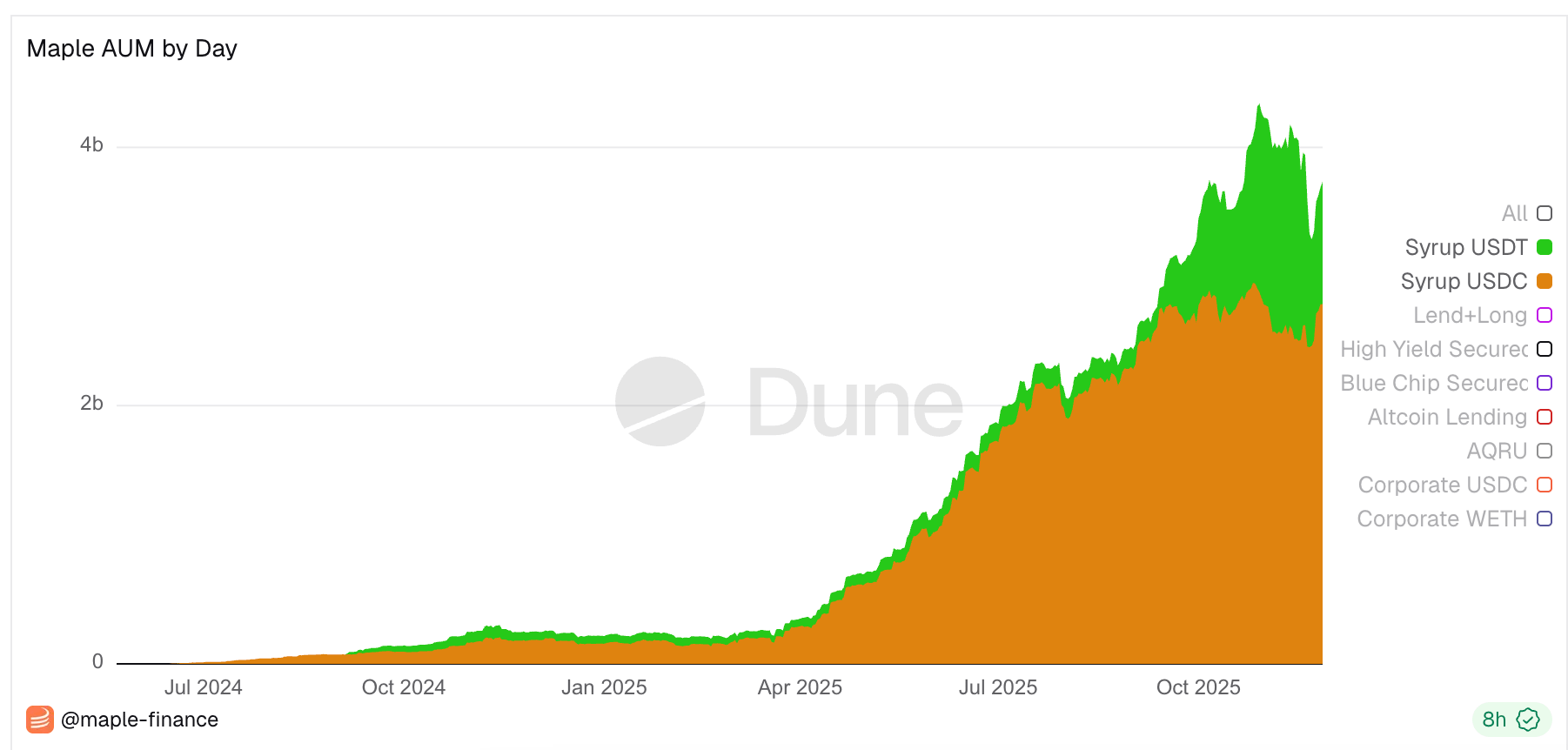

Maple had to shift their focus from the “trust-based” model to cope with the market. They launched Maple Direct and Syrup, moving effectively into on-chain prime brokerage.

The new model minimizes the enforcement gap by demanding strict over-collateralization. They stopped trying to fix the recovery problem and simply removed the risk.

2. Goldfinch

Goldfinch suffered a different, but equally painful, lesson. Their mission was noble: “Crypto loans for emerging markets.”

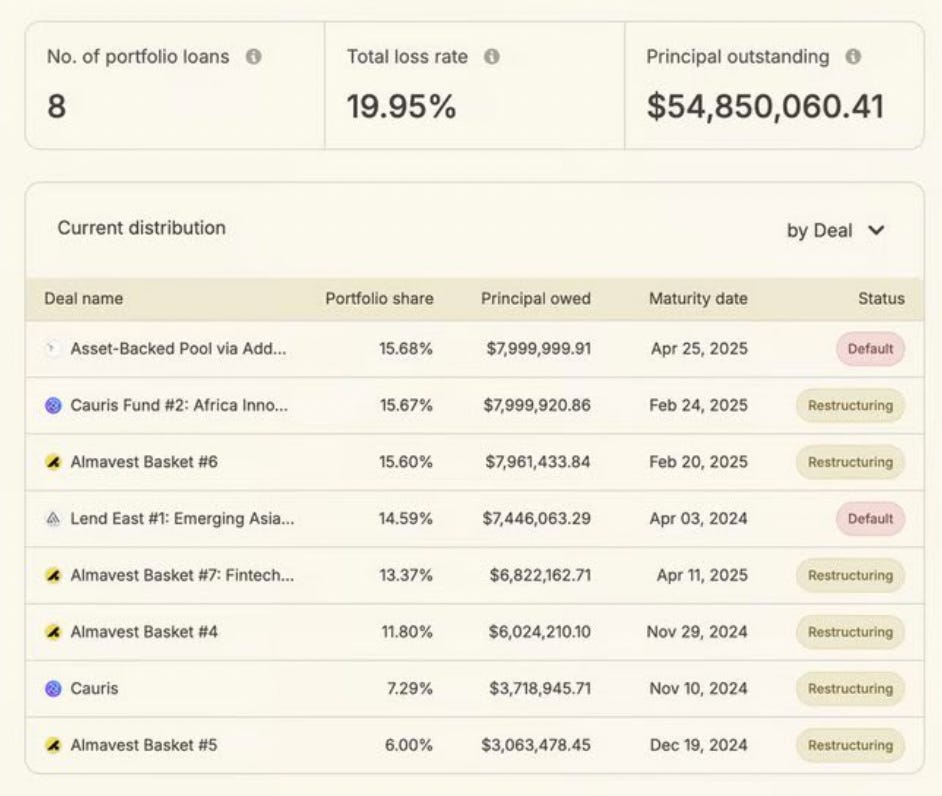

Predictably, they faced several defaults from companies in a short period of time. Most notably, Tugende ($5M), Stratos (~$7M), and Lend East. The break point was the Lend East default. A borrower with a $10.2 million loan could only repay $4.25 million.

Goldfinch realized that no amount of on-chain governance could fix a bad off-chain business model.

As a pivot from this model, in 2025, Goldfinch executed the Goldfinch Prime maneuver. They stopped trying to be the underwriter for SMEs in Kenya. Instead, they became a fund of funds.

They onboarded credit managers from BlackRock’s HPS, Crescent, and Monroe Capital. The logic is a complete admission of defeat regarding crypto-native risk assessment.

Basically adopting the attitude that since we cannot do underwriting better than BlackRock, let’s just build the rails for BlackRock to get liquidity from crypto.

It’s important to note that currently, all 8 loans in Goldfinch’s Senior Pool are in distress.

All I could find was some messages from their Chief Restructuring Officer saying they are in active negotiations with a few of the defaulters. The messages didn’t include any proof or documentation of the negotiation process. I checked their Discord to understand what steps are being taken for fund recovery/collection, as they claim the loans are backed by Real World Assets and are legally pursuable.

3. Clearpool

Clearpool, on the other hand, doubled down on market dynamics.

They introduced Dynamic Interest Rates. Borrowing from the Aave utilization curve, Clearpool’s algorithm adjusts rates based on the demand for liquidity in specific borrower pools.

This creates a fluid market. Instead of the fixed-term, fixed-rate loans that locked Maple into bad positions, Clearpool rates price risk in real-time. As of late 2025, they are facilitating loans to firms like Hyperithm, eliminating liquidation risk for borrowers (no collateral to sell) in exchange for significantly higher yields for lenders.

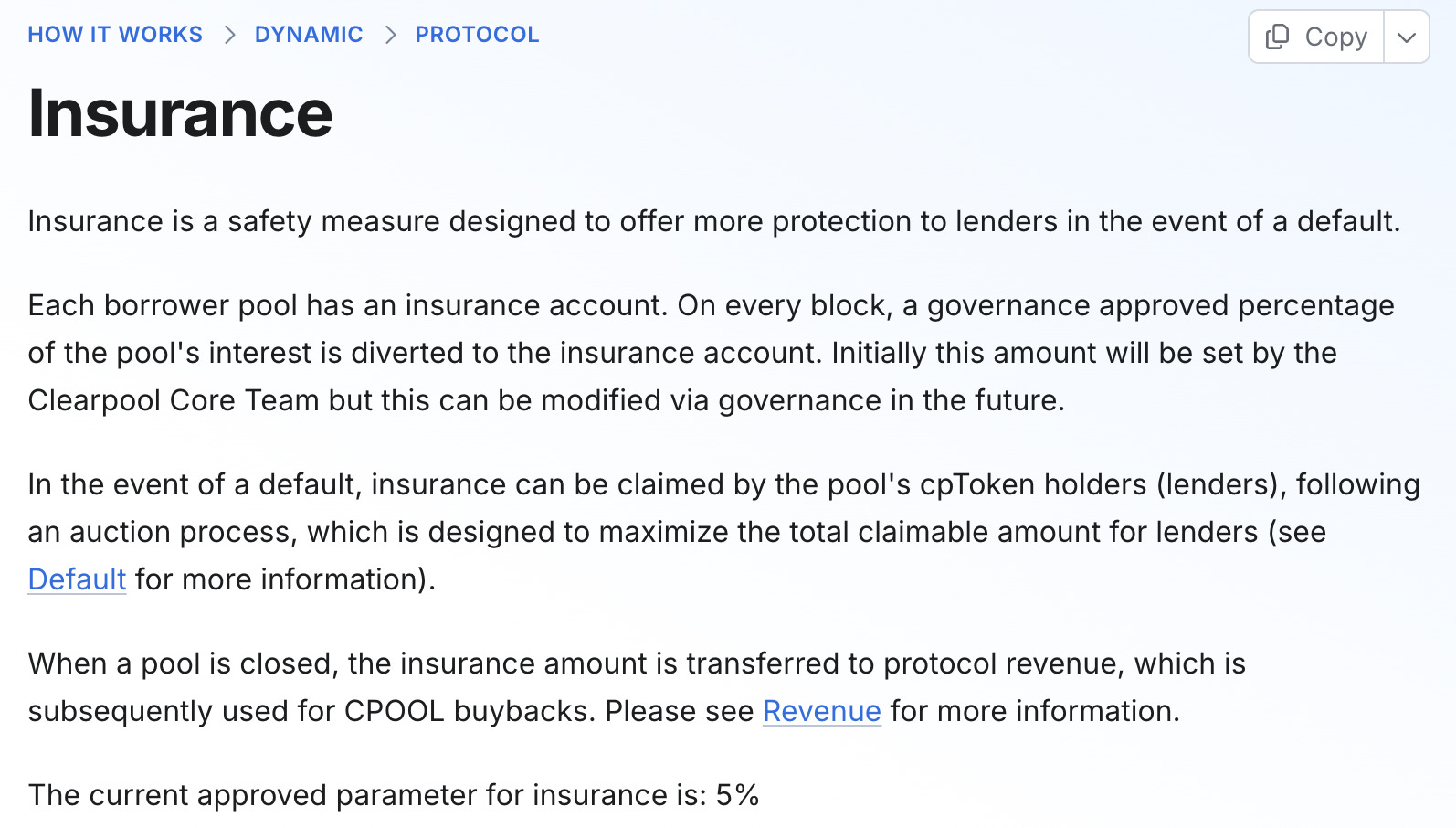

What I found most interesting is their debt recovery process which includes an insurance component.

Clearpool auctions off its bad debt to collection agencies who retain the right to legally pursue the defaulters just like in TradFi. On top of it, every pool has a reserved 5% insurance quota that gets distributed among lenders in the event of a default.

While this doesn’t make the lenders whole, it does add a layer of certainty that other uncollateralized lending protocols lack.

4. Credit Coop

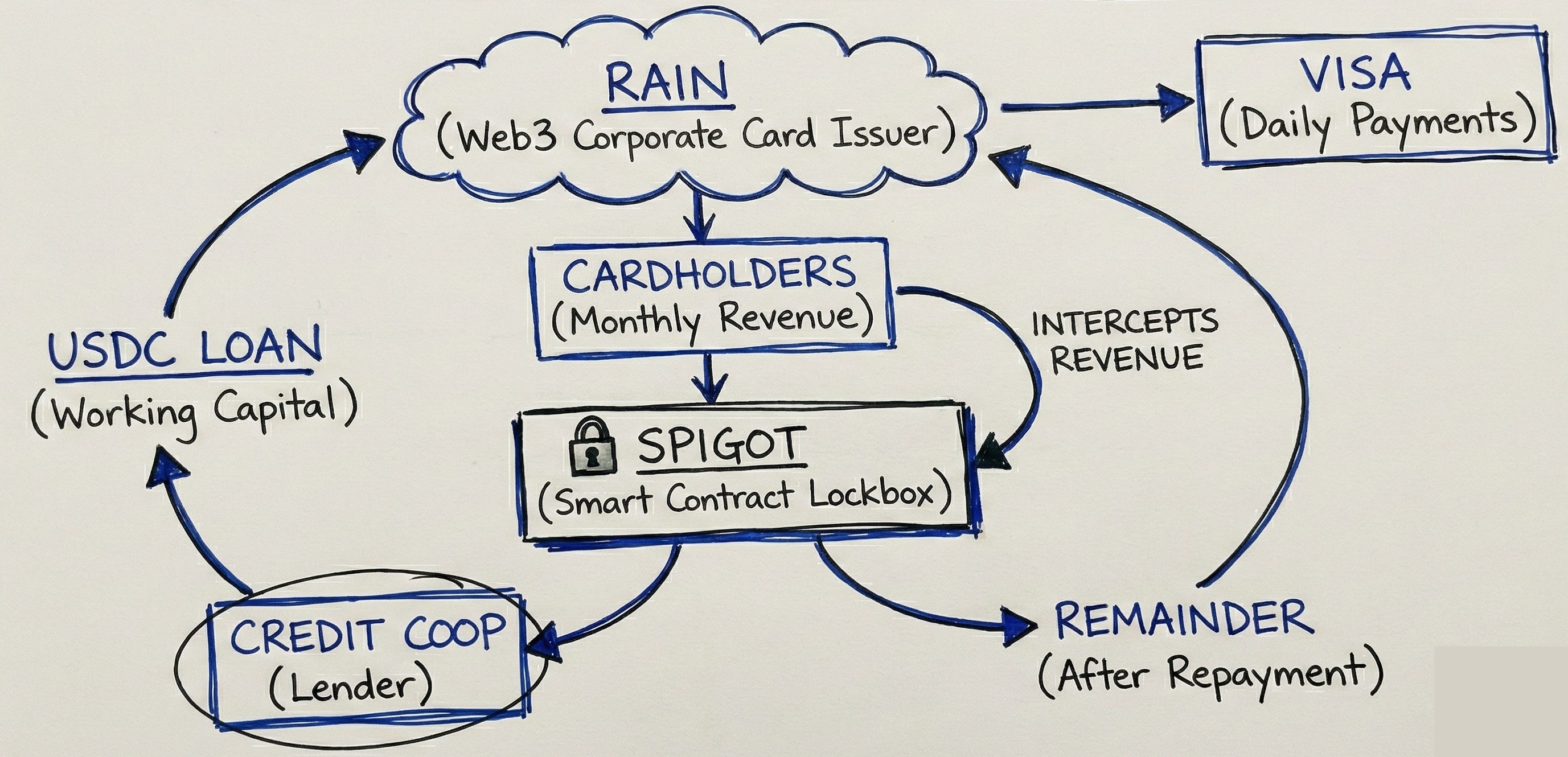

Credit Coop has taken a different approach to solve the debt recovery problem with their Spigot smart contract.

The Spigot is basically a programmable lockbox. It acts as middleware between a borrower’s revenue source and their wallet.

How it works:

Escrow: The Spigot intercepts the borrower’s on-chain revenue (from payment processors, invoices, or other smart contracts).

Split: It automatically takes the loan repayment first.

Remit: The borrower only gets the remainder.

How Rain is Using Credit Coop

You can see this model in action in Credit Coop’s integration with Rain, a corporate card issuer for Web3 companies.

The Problem: Rain owes Visa money daily for card swipes. But Rain doesn’t collect from cardholders until the end of the month. This is a massive working capital gap.

The Solution: Rain borrows USDC from Credit Coop against their future receivables to pay Visa.

The Security: The Spigot intercepts the future receivables from the cardholders.

By August 2025, Rain was moving $175 million monthly through this pipe. Zero defaults. This is by far the best innovation we have seen in the crypto lending landscape when it comes to default and debt recovery.

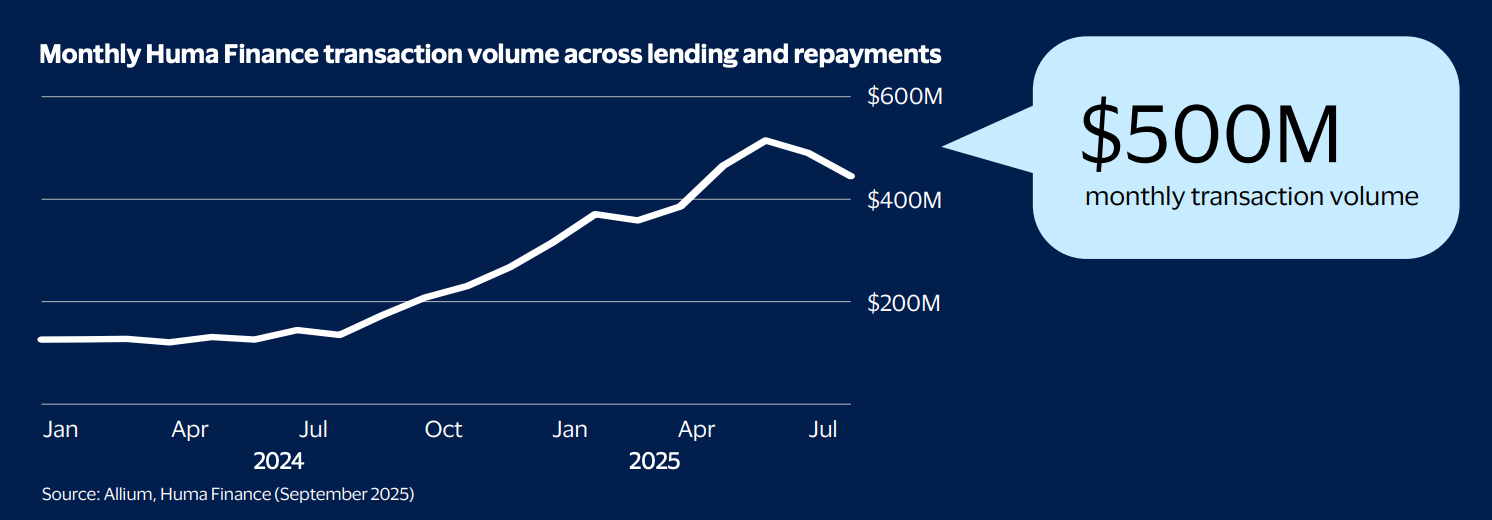

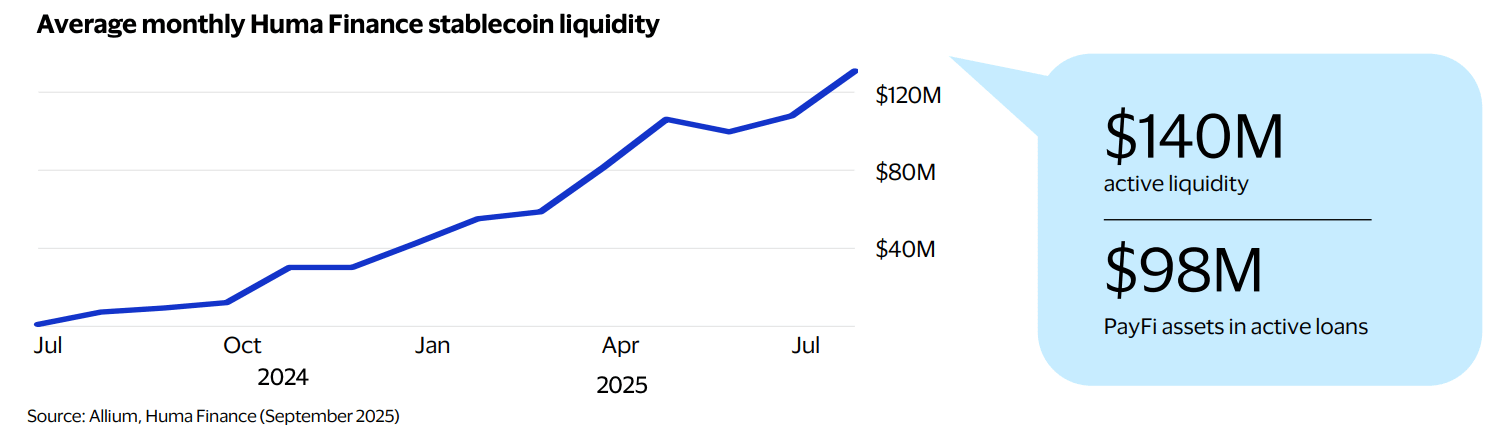

5. Huma Finance

While Credit Coop builds the plumbing, Huma Finance is building the PayFi Network.

Consider a cross-border remittance. A company in Mexico needs to pay out Pesos now, but the Dollars from the US sender haven’t settled yet. This creates a liquidity gap of perhaps 24 hours.

Huma swoops in to save the day by lending USDC to the payment processor. It’s a high velocity environment with ultra-short-term loan duration, a perfect problem for stablecoin to solve.

Huma is generating upwards of 10% yield recycling short-term (daily or even hourly) debt to high cashflow businesses.

By April 2025, Huma surpassed $4 billion in Total Transaction Volume (TTV) in partnership with Arf (a global settlement platform).

Building Onchain Credit Score

By now, you understand the primary problems with unsecured lending in crypto:

Creditworthiness – Lack of a reliable credit scoring system

Regulation – Lack of trust in the system

Legal Recourse – Lack of clear guidelines in the event of a default

Creditworthiness is the foremost obstacle to address. If you can analyze the borrower’s financial activities, both off and on chain, and run a risk analysis on their overall financial health, while ensuring they are in a jurisdiction suitable for legal pursuit, the decision making process gets a lot easier.

Thankfully, there are a few companies working on it.

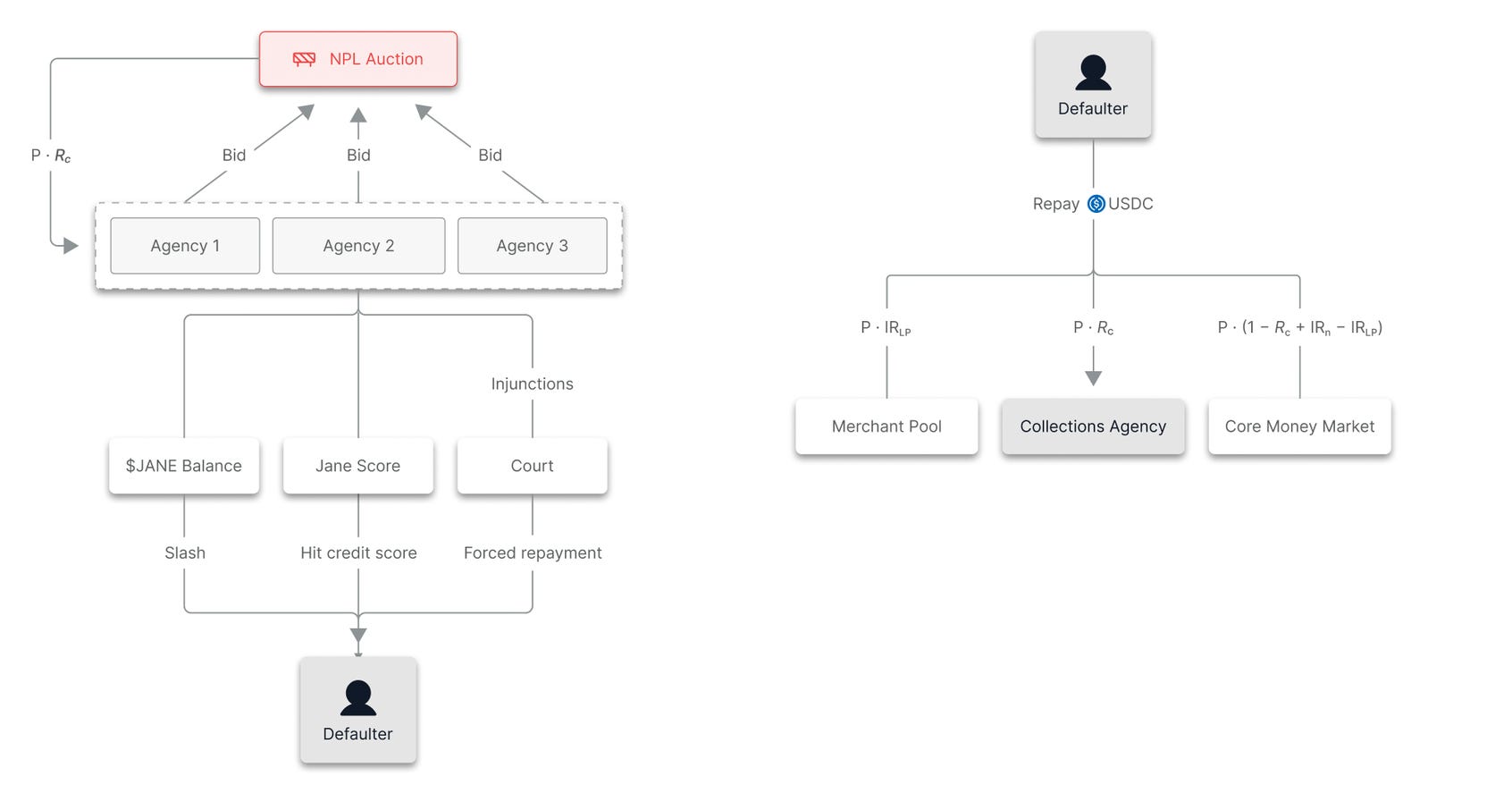

3Jane

3Jane is attempting to bring the unsecured credit to individuals or small traders using zkTLS (Zero-Knowledge Transport Layer Security).

This addresses the “Privacy-Verification Paradox”: borrowers have data (bank balances, credit scores, trading history) that proves they are creditworthy, but they cannot put that data on a public blockchain due to privacy and security concerns.

3Jane uses zkTLS to allow users to generate a proof of their off-chain data without revealing the data itself.

Connection: Users connect their bank accounts or CEX accounts (like Coinbase or Binance) to their browser.

Proof Generation: The zkTLS protocol intercepts the TLS session between the user and the bank/exchange. It verifies the data (e.g., “This user has >$10,000 in X Bank”) and generates a Zero-Knowledge Proof.

On-Chain Verification: The 3Jane protocol verifies the proof on-chain. The smart contract sees only “True” or “False,” not the bank balance or login credentials.

Credit Issuance: Based on this verified data, the protocol issues a credit line in USD3, a stablecoin/credit token backed by the pool of loans.

Credora is another company that calculates risk scores by monitoring a borrower’s positions across CEXs and DeFi in real-time.

It allows a protocol like Morpho to say: “We will lend you money, but if your risk score on Binance drops below 600, we liquidate you automatically.” This commoditizes risk data. Credit scores are now just another oracle feed.

The Ultimate Unsecured Lending Stack

The answer to swallow the US unsecured credit market isn’t one-size-fits-all. We have to answer a number of questions and put backstops in places that allow businesses to trust crypto loans and for crypto lenders to trust the borrowers.

I have laid out the primary obstacles as I see them. To solve them, we need to deploy the Ultimate Unsecured Lending Stack.

The Stack consists of 3 layers:

Financial incentives that align with the borrowers’ expectations and the lenders’ risk profile

A system to analyze and verify borrowers’ creditworthiness and overall financial health.

Favor borrowers from crypto friendly jurisdictions where a legal pursuit is feasible.

If a lending protocol satisfies all 3 layers of the stack, it radically minimizes the absurd amount of risk lenders bear in the current unsecured lending landscape.